》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

SMM News on June 12:

PV aluminum extrusion: This week, the operating rates of PV frame sample enterprises continued to diverge. Production cuts at downstream module plants have become a certainty. Affected by this, the operating rates of some PV frame extrusion enterprises in east China and Hebei continued to decline. However, according to SMM, some small and medium-sized PV frame extrusion enterprises in south-west China maintained high operating rates, mainly because their spraying production line capacity was basically in line with the procurement demand of leading module plants, and their operations remained at full capacity.

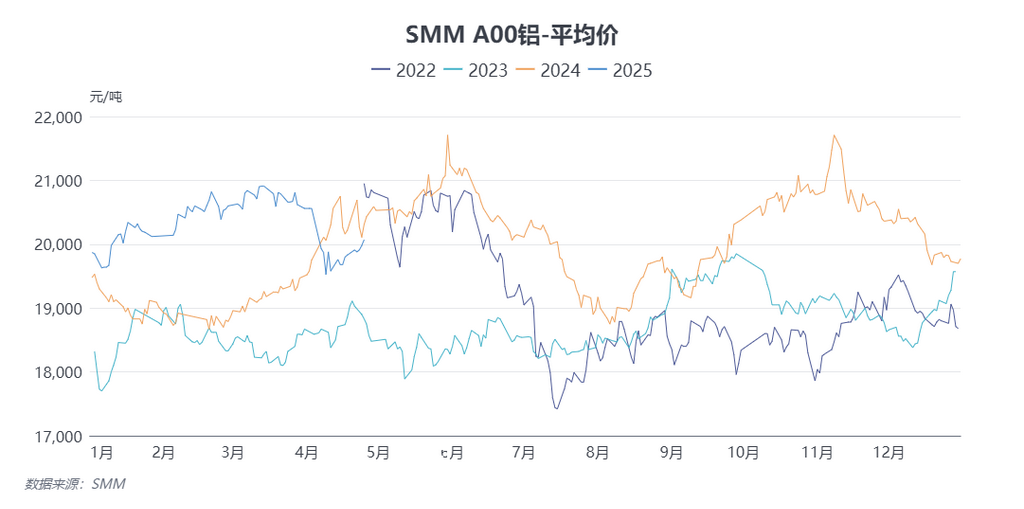

Raw material prices: During the period (June 9, 2025 - June 12, 2025), the center of the average spot price of spot aluminum moved upward. The SMM A00 weekly average price was 20,355 yuan/mt, up 0.68% from the previous weekly average. On the macro front, the US core CPI was lower than expected, raising market expectations for a US Fed interest rate cut in September. China and the US reached a consensus in principle on the framework of measures to implement and consolidate the outcomes of the Geneva economic and trade talks. However, market concerns about the future economic outlook remained, with macro sentiment generally neutral to cautious. Domestic operating capacity of electrolytic aluminum remained stable. It should be noted that with the weakening of aluminum billet consumption, processing fees have continued to decline, and expectations for an increase in casting ingot production at month-end have emerged. However, in the short term, the domestic market will still maintain an ultra-low inventory level. On the cost side, the real-time cost of electrolytic aluminum increased slightly by 18 yuan/mt WoW to 17,199 yuan/mt, and domestic aluminum smelters maintained a high-profit status. Demand side, with the onset of the off-season, shipments of downstream wrought aluminum enterprises have declined, leading to an accumulation of finished product inventories. Some wrought aluminum enterprises have already begun to cut production and reduce loads. According to SMM observations, most terminal consumption sectors have not yet shown a super-seasonal weakening. However, caution should be exercised as the high aluminum prices may further dampen consumption. The inventory port is currently the biggest contradiction in the aluminum fundamentals. Historically low domestic and overseas inventories have strengthened the price spread between futures contracts and fueled absolute prices. The low inventory status is difficult to change in the short term. From a seasonal perspective in previous years, aluminum ingot inventories have tended to destock in most months of June. Overseas, there is a risk of re-transferring to delivery warehouse to the LME in the next 2-3 weeks after a decline in large holders' open interest. The inventory port is currently the biggest contradiction in the aluminum fundamentals. Historically low domestic and overseas inventories have strengthened the price spread between futures contracts and fueled absolute prices. The low inventory status is difficult to change in the short term. From a seasonal perspective in previous years, aluminum ingot inventories have tended to destock in most months of June. Overseas, there is a risk of re-transferring to delivery warehouse to the LME in the next 2-3 weeks after a decline in large holders' open interest. According to SMM statistics, low domestic arrivals still support the destocking trend. After the rapid breakthrough of the 500,000 mt threshold, there is still room for further decline. It is expected that aluminum prices will hold up well in the short term. Next week, SHFE aluminum is expected to trade within the range of 20,200-20,700 yuan/mt. If it can hold above 20,500 yuan/mt technically, it is expected to test the resistance level at 21,000 yuan/mt. LME aluminum is expected to trade within the range of $2,470-2,570/mt. After breaking through the key resistance level of $2,450/mt, LME aluminum is expected to hold up well.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)